The NY state income tax rate is a critical aspect of financial planning for residents and non-residents who work in or earn income from New York State. Understanding this tax rate is essential for accurate tax filing and financial management. With its progressive tax system, New York imposes varying rates based on income levels, influencing taxpayers' financial obligations significantly. Navigating these rates can often be complex, requiring a clear comprehension of the underlying rules and regulations. This guide aims to provide a comprehensive overview of the NY state income tax rate, offering insights into its structure, implications, and strategies for effective tax planning.

New York State's income tax rates are structured in a progressive manner, meaning that the percentage of tax increases as the taxpayer's income rises. This system is designed to ensure that those with higher incomes contribute a larger share of their earnings in taxes. For residents and those with New York-sourced income, understanding the details of these rates is crucial to avoid any potential penalties or surprises during tax season. The state also provides various deductions and credits that can significantly impact the final tax liability, making it beneficial to be well-informed.

Whether you are a resident, a part-year resident, or a non-resident earning income in New York, this guide will delve into the specifics of the NY state income tax rate. We will explore the current tax brackets, rates, and any recent changes in legislation that may affect taxpayers. Additionally, we'll provide practical advice on filing taxes, potential deductions, and credits, along with strategies to minimize tax liabilities. Armed with this knowledge, taxpayers can approach their tax obligations with confidence and ensure compliance with state laws.

Table of Contents

- What is the NY State Income Tax Rate?

- How Does the Progressive Tax System Work?

- Current Tax Brackets and Rates

- What Factors Influence the NY State Income Tax Rate?

- Residency Status and Its Impact on Taxation

- Tax Credits and Deductions Available

- Filing Requirements and Process

- Strategies to Minimize Tax Liability

- How to Handle Tax Discrepancies and Audits?

- Impact of Recent Legislative Changes

- Common Mistakes to Avoid

- How Does the NY State Income Tax Rate Compare with Other States?

- Frequently Asked Questions

- Conclusion

What is the NY State Income Tax Rate?

The NY state income tax rate is a set of rates imposed on the income earned by individuals within the state. It's essential to understand that New York uses a progressive tax system, meaning that as your income increases, so does your tax rate. This system aims to ensure fairness, as those with higher incomes are expected to contribute a larger portion of their earnings towards state funding. The rates can range from as low as 4% to as high as 10.90%, depending on an individual's income bracket. It's crucial for taxpayers to know which bracket they fall into to properly calculate their tax liability.

How Tax Rates are Determined

The determination of tax rates in New York is based on several factors, including income level, filing status, and residency status. The state legislature periodically reviews and adjusts these rates to align with economic conditions and budgetary needs. As a taxpayer, staying informed about these changes is essential to ensure accurate tax calculations and compliance with state laws.

Progressive Tax System

New York's progressive tax system is designed to ensure that taxpayers contribute a fair share based on their ability to pay. This means that as your income increases, the percentage of income you pay in taxes also increases. For example, lower-income individuals might fall into the 4% bracket, while higher-income earners can be taxed up to 10.90% of their income. Understanding where you stand within these brackets is crucial for effective tax planning and management.

How Does the Progressive Tax System Work?

The progressive tax system is structured to impose higher rates on higher income levels, making it a fair approach to taxation. In New York, this system is applied to various income brackets, ensuring that wealthier individuals contribute more to state revenue. The idea is to distribute the tax burden more equitably, allowing those with lower incomes to retain a larger portion of their earnings. This section will delve into how this system operates and the implications it has for different income groups.

Income Brackets and Tax Rates

New York's income tax brackets determine the percentage of tax applied to different portions of an individual's income. These brackets vary according to filing status, such as single, married filing jointly, or head of household. Each bracket has a specific rate, which increases as income rises. It's important for taxpayers to understand which bracket they fall into to accurately calculate their taxes. The brackets are adjusted annually to account for inflation and changes in the economic landscape.

Impact on Taxpayers

The progressive nature of the NY state income tax rate means that taxpayers with higher incomes bear a larger tax burden. This system is designed to ensure social equity by redistributing wealth. However, it can also lead to higher tax bills for those in the upper brackets. Taxpayers need to be aware of their bracket and plan accordingly to manage their financial obligations effectively. Utilizing available deductions and credits can help mitigate the impact of higher rates.

Current Tax Brackets and Rates

The current tax brackets and rates in New York are crucial for taxpayers to understand, as they directly affect the amount of tax owed. These brackets are determined by the New York State Department of Taxation and Finance and are subject to annual updates. Knowing the current rates and brackets helps taxpayers accurately calculate their liabilities and plan for future tax obligations.

- 4%: Applies to income up to $8,500 for single filers, $12,800 for married filing jointly, and $17,150 for heads of household.

- 4.5%: Applies to income between $8,501 and $11,700 for single filers, $12,801 and $17,150 for married filing jointly, and $17,151 and $22,600 for heads of household.

- 5.25%: Applies to income between $11,701 and $13,900 for single filers, $17,151 and $23,600 for married filing jointly, and $22,601 and $30,000 for heads of household.

- 5.85%: Applies to income between $13,901 and $21,400 for single filers, $23,601 and $44,000 for married filing jointly, and $30,001 and $60,000 for heads of household.

- 6.25%: Applies to income between $21,401 and $80,650 for single filers, $44,001 and $107,650 for married filing jointly, and $60,001 and $107,650 for heads of household.

- 6.85%: Applies to income between $80,651 and $215,400 for single filers, $107,651 and $269,300 for married filing jointly, and $107,651 and $215,400 for heads of household.

- 9.65%: Applies to income between $215,401 and $1,077,550 for single filers, $269,301 and $1,616,450 for married filing jointly, and $215,401 and $1,077,550 for heads of household.

- 10.3%: Applies to income between $1,077,551 and $5,000,000 for single filers, married filing jointly, and heads of household.

- 10.9%: Applies to income over $5,000,000 for single filers, married filing jointly, and heads of household.

What Factors Influence the NY State Income Tax Rate?

Several factors influence the NY state income tax rate, including economic conditions, legislative decisions, and public policy considerations. These factors can lead to adjustments in tax rates and brackets, impacting taxpayers' financial responsibilities. Understanding these influences can help taxpayers anticipate changes and adjust their financial planning accordingly.

Legislative Changes

Legislative changes are a significant factor in determining the NY state income tax rate. The state legislature reviews and adjusts tax rates and brackets to align with budgetary needs, economic conditions, and public policy goals. These changes can lead to increases or decreases in tax rates, affecting taxpayers' obligations. Staying informed about legislative developments is crucial for accurate tax planning.

Economic Conditions

Economic conditions play a vital role in shaping the NY state income tax rate. During economic downturns, the state may adjust tax rates to generate additional revenue, while periods of growth may lead to rate reductions. Taxpayers need to be aware of these economic influences to anticipate potential changes in their tax liabilities and plan accordingly.

Residency Status and Its Impact on Taxation

Residency status is a critical factor in determining an individual's tax obligations in New York. The state classifies taxpayers as residents, part-year residents, or non-residents, each with different tax responsibilities. Understanding your residency status is essential for accurate tax filing and compliance with state laws.

Resident Taxation

Residents of New York are subject to state income tax on all their income, regardless of where it's earned. This includes income from out-of-state sources. To be considered a resident, an individual must either maintain a permanent home in New York or spend more than 183 days in the state during the tax year. Properly determining residency status is crucial to avoid potential penalties and ensure compliance with state tax laws.

Non-Resident and Part-Year Resident Taxation

Non-residents and part-year residents are only taxed on income earned from New York sources. For non-residents, this includes income from employment, business operations, or property within the state. Part-year residents, on the other hand, are taxed as residents for the portion of the year they lived in New York and as non-residents for the remaining period. Accurately determining your residency status and understanding the associated tax implications are essential for compliance and effective tax planning.

Tax Credits and Deductions Available

New York offers various tax credits and deductions to help taxpayers reduce their overall tax liability. These provisions can provide significant savings, making it essential for taxpayers to understand and utilize them effectively. This section will explore the available credits and deductions and their impact on the NY state income tax rate.

Common Tax Credits

New York offers several tax credits, including the Earned Income Tax Credit (EITC), Child and Dependent Care Credit, and the New York State College Tuition Credit. These credits are designed to provide financial relief to eligible taxpayers and can significantly reduce the amount of tax owed. Understanding the eligibility criteria and application process for these credits is crucial for maximizing tax savings.

Available Deductions

In addition to credits, New York provides various deductions that can lower taxable income and reduce tax liability. Common deductions include those for mortgage interest, student loan interest, and medical expenses. Taxpayers should carefully review their eligibility for these deductions and maintain accurate records to support their claims. Utilizing these deductions can lead to substantial savings and a lower overall tax bill.

Filing Requirements and Process

Understanding the filing requirements and process for New York State taxes is essential for ensuring compliance and avoiding potential penalties. This section will guide taxpayers through the necessary steps for filing their state income tax returns accurately and efficiently.

Who Needs to File?

Individuals who earn income in New York, whether as residents, part-year residents, or non-residents, may be required to file a state income tax return. The specific filing requirements depend on income level, residency status, and filing status. Taxpayers should review the state's guidelines to determine their filing obligations and ensure they submit their returns on time.

Filing Process

The filing process for New York State taxes involves several steps, including gathering necessary documentation, completing tax forms, and submitting returns to the New York State Department of Taxation and Finance. Taxpayers can file electronically or by mail, with electronic filing offering several benefits, such as faster processing and quicker refunds. Ensuring accuracy and completeness in the filing process is crucial to avoid delays and potential penalties.

Strategies to Minimize Tax Liability

Minimizing tax liability is an important aspect of financial planning for taxpayers in New York. By implementing effective strategies, individuals can reduce their overall tax burden and increase their financial savings. This section will explore various approaches to minimizing tax liability in the state.

Tax Planning

Tax planning involves analyzing your financial situation and making strategic decisions to optimize tax outcomes. This may include timing income and expenses, maximizing deductions and credits, and utilizing tax-advantaged accounts. By carefully planning your tax strategy, you can reduce your liability and increase your savings.

Utilizing Credits and Deductions

Taking full advantage of available tax credits and deductions is a key strategy for minimizing tax liability. By understanding the eligibility criteria and application process for these provisions, taxpayers can significantly reduce their taxable income and overall tax bill. Proper documentation and record-keeping are essential for claiming these benefits.

How to Handle Tax Discrepancies and Audits?

Tax discrepancies and audits can be a source of stress for taxpayers, but understanding how to handle them can alleviate concerns and ensure compliance. This section will explore the steps to take when facing discrepancies or audits and how to resolve them effectively.

Identifying and Resolving Discrepancies

If you discover discrepancies in your tax return, it's important to address them promptly to avoid potential penalties. This may involve reviewing your records, amending your return, and communicating with the New York State Department of Taxation and Finance. Understanding the cause of the discrepancy and taking corrective action is crucial for resolving the issue.

Preparing for Audits

Being prepared for a tax audit involves maintaining accurate records and documentation to support your tax return. If selected for an audit, you will need to provide evidence to substantiate your claims and resolve any issues identified by the tax authorities. Understanding the audit process and knowing your rights as a taxpayer can help you navigate this experience successfully.

Impact of Recent Legislative Changes

Recent legislative changes can have a significant impact on the NY state income tax rate and taxpayers' obligations. Staying informed about these changes is crucial for accurate tax planning and compliance. This section will explore the recent developments in New York tax legislation and their implications for taxpayers.

Key Legislative Developments

Recent legislative changes in New York may include adjustments to tax rates, brackets, credits, and deductions. These changes can affect taxpayers' liabilities and filing requirements, making it essential to stay informed and adjust your tax strategy accordingly. Understanding these developments can help you anticipate changes and plan for the future.

Implications for Taxpayers

Legislative changes can have various implications for taxpayers, including increased or decreased tax liabilities, changes in filing requirements, and adjustments to available credits and deductions. Being aware of these changes and understanding their impact on your tax situation can help you make informed decisions and optimize your tax outcomes.

Common Mistakes to Avoid

Avoiding common mistakes is essential for accurate tax filing and compliance with New York State tax laws. This section will explore the typical errors taxpayers make and how to prevent them, ensuring a smooth and successful tax filing experience.

Errors in Tax Returns

Common errors in tax returns include incorrect calculations, missing information, and failure to attach necessary documentation. These mistakes can lead to delays, penalties, and even audits. Reviewing your return carefully and double-checking all information before submission can help prevent these issues.

Neglecting Credits and Deductions

Failing to take advantage of available credits and deductions is a common mistake that can lead to higher tax liabilities. Taxpayers should be aware of the credits and deductions they qualify for and ensure they claim them correctly on their tax return. Proper documentation and record-keeping are essential for supporting these claims.

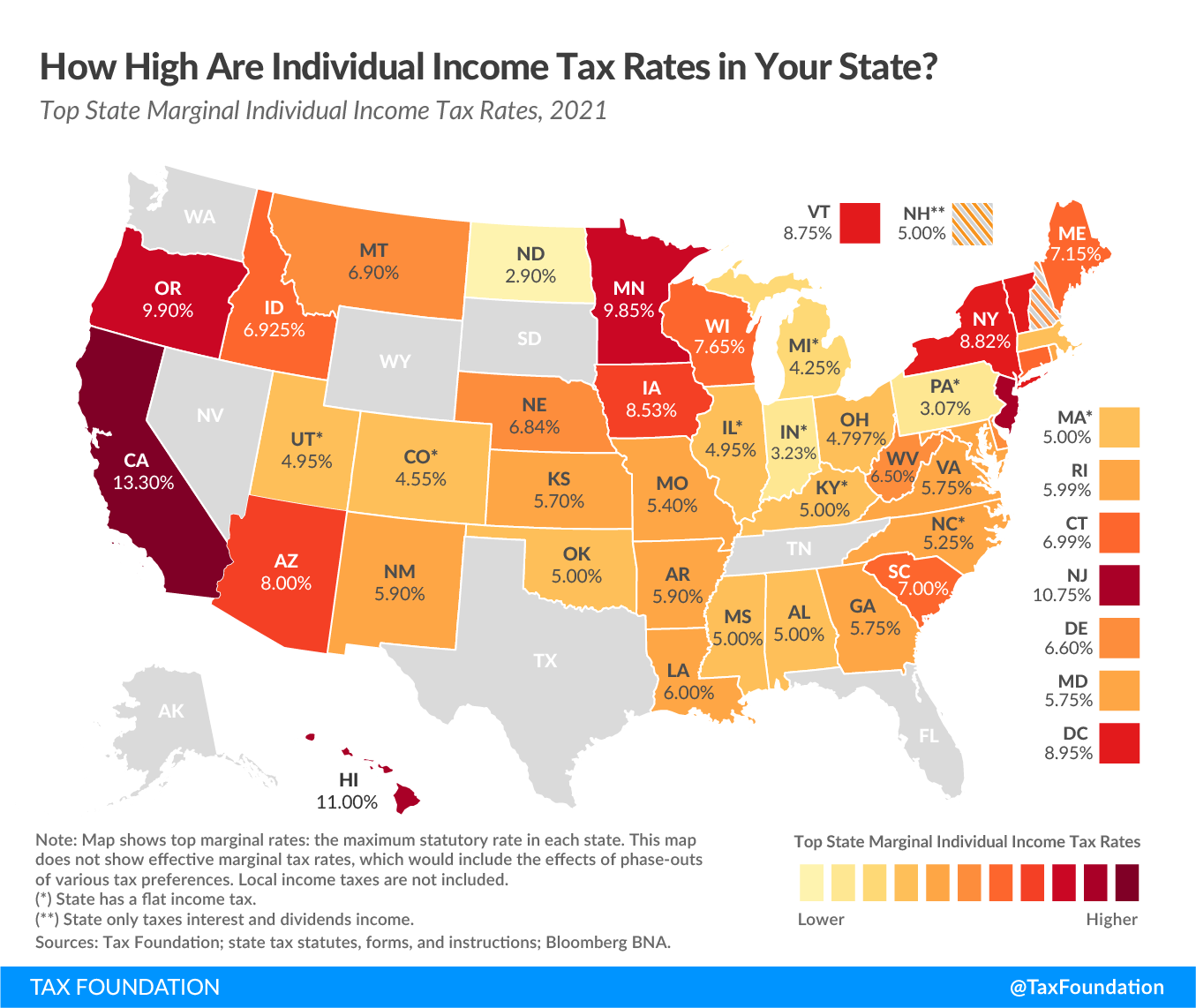

How Does the NY State Income Tax Rate Compare with Other States?

Comparing the NY state income tax rate with other states can provide valuable insights into the state's tax policies and their impact on taxpayers. This section will explore how New York's tax rates stack up against those of other states and what this means for residents and non-residents.

Comparison with Neighboring States

New York's income tax rates are generally higher than those of its neighboring states, such as New Jersey and Connecticut. This can make New York a more expensive state for taxpayers, particularly those in higher income brackets. Understanding these differences can help taxpayers make informed decisions about residency and financial planning.

Impact on Taxpayers

The higher tax rates in New York can lead to increased financial burdens for residents and non-residents earning income in the state. Taxpayers need to be aware of these rates and plan accordingly to manage their financial obligations effectively. Utilizing available credits and deductions can help mitigate the impact of higher rates and reduce overall tax liabilities.

Frequently Asked Questions

Here are some frequently asked questions regarding the NY state income tax rate and their answers to help taxpayers better understand their obligations and rights.

1. What is the highest income tax rate in New York State?

The highest income tax rate in New York State is 10.90%, applicable to income over $5,000,000 for single filers, married filing jointly, and heads of household.

2. Are there any tax credits available for New York State taxpayers?

Yes, New York State offers several tax credits, including the Earned Income Tax Credit (EITC), Child and Dependent Care Credit, and the New York State College Tuition Credit.

3. How can I determine my residency status for New York State taxes?

Your residency status is determined based on whether you maintain a permanent home in New York or spend more than 183 days in the state during the tax year.

4. What should I do if I receive a tax audit notice from New York State?

If you receive a tax audit notice, you should review the notice carefully, gather supporting documentation, and respond promptly to address any issues identified by the tax authorities.

5. Can I file my New York State taxes electronically?

Yes, you can file your New York State taxes electronically using the state's online filing system, which offers benefits such as faster processing and quicker refunds.

6. How do recent legislative changes affect my New York State tax obligations?

Recent legislative changes can affect your tax obligations by adjusting tax rates, brackets, credits, and deductions. Staying informed about these changes is essential for accurate tax planning and compliance.

Conclusion

Understanding the NY state income tax rate is crucial for effective financial planning and compliance. With its progressive tax system, New York imposes varying rates based on income levels, influencing taxpayers' financial obligations significantly. By staying informed about the current tax brackets, rates, and legislative changes, taxpayers can approach their tax obligations with confidence. Utilizing available credits and deductions, planning strategically, and avoiding common mistakes can help taxpayers minimize their tax liability and ensure a smooth and successful tax filing experience. Ultimately, being well-informed and proactive in managing your tax responsibilities can lead to greater financial stability and peace of mind.

You Might Also Like

Vegamovies NL: Your Ultimate Guide To Seamless Streaming ExperienceMovierulz 2023 -- Download: A Comprehensive Guide And Insights

Memorable Moments Of Joshua Hill And Melissa Murray Wedding Extravaganza

Unmissable Drama And Passion: Hot Web Series Ullu

Alanna Panday: A Rising Star In The World Of Fashion And Social Media

Article Recommendations